What is a Balance Transfer?

Shifting your Home Loan/Loan Against Property/Business Loan Account from one Bank/HFC (Housing Finance Company) to another Bank/HFC is called a ‘Balance Transfer (BT)’ facility.

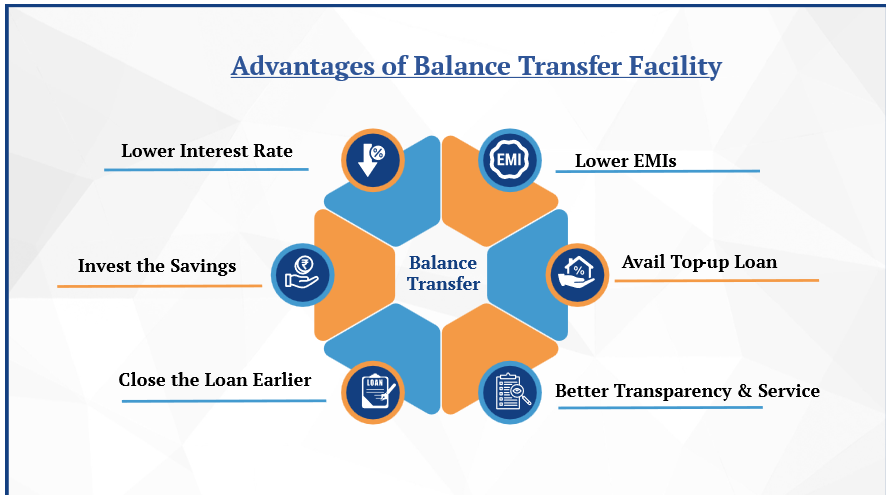

Why Balance Transfer?

Following are the important advantages of opting for a Balance Transfer facility explained in the illustration below.

Illustration:

Mr. Ashok is servicing a Home Loan at 9.35% interest with an EMI of Rs. 87,992. The outstanding loan is Rs. 85 Lakhs, and the balance repayment is 180 months (15 years).

Another Bank has offered a Balance Transfer facility to take over the outstanding loan at 8.35% interest with an EMI of Rs. 82,958 for the same repayment tenure of 180 months.

| ILLUSTRATION | LOAN AMOUNT | INTEREST | TENURE | EMI |

| EXISTING LOAN | Rs. 85 LAKHS | 9.35% | 15 YEARS | Rs. 87,992 |

| BALANCE TRANSFER LOAN | Rs. 85 LAKHS | 8.35% | 15 YEARS | Rs. 82,958 |

1. Lower Interest: The foremost advantage is the lower interest charged by the Bank or HFC that is willing to take over the existing Home Loan, LAP, or business Loan from another Bank or HFC.

In the illustration above, the reduction in the interest rate is 1%.

2. Lower EMIs: The reduction in interest manifests as either a lower EMI (retaining the existing repayment tenure) or a reduction in the existing repayment tenure, at the borrower’s choice.

In the illustration, the EMI gets reduced by Rs. 5,034. A 1% reduction in interest reduces the EMI by 5.72%! Thus, the total savings over 15 years will be Rs. 9,06,120.

3. Invest the Savings: If you opt for the lower EMI, you will have a golden opportunity to invest the savings (existing EMI – new EMI) in safe and secure schemes such as SIP (Systematic Investment Plan) and similar schemes.

In the illustration, the investment of Rs. 5,000 made every month in SIP/similar Scheme over 15 years will yield Rs. 21.03 lakhs at a modest 10% interest.

4. Avail Top-up Loan: If you are in need, you can get a considerable Top-up loan, without increasing the existing EMI.

In the illustration, Mr. Ashok opted for a Top-up Loan of Rs. 5 Lakhs at 8.35% interest, at a total EMI of Rs. 87,838, less than the existing EMI of Rs. 87,992.

5. Repay the Loan Earlier: By continuing to pay the existing EMIs, the repayment tenure reduces by many months earlier, thus saving a lot of money.

In the illustration, by continuing to pay the existing EMIs, the loan closes 19/20 months earlier, thus a saving of Rs. 16.7 Lakhs.

6. Better Transparency & Service: You need to select a Bank/HFC that offers not only lesser interest rates on the Balance Transfer but which has established transparency in dealing and maintained the best service standards.

Advantages of Balance Transfer for your existing Home Loan/LAP/Business Loan:

To find out the savings on your existing Home Loan/LAP/Business Loan, just contact us with the LATEST LOAN STATEMENT. We will provide a customized computation sheet explaining the exact savings on EMIs, Top-up Loans, Loan Pre-closures, and creating a huge corpus by investing the savings, etc.

We guide you on:

Financial benefits of transferring your Home Loan/Loan Against Property/Business Loan to another Bank or HFC (Housing Finance Company) that offers better Interest Rates, Top-up Loans, and many more favourable benefits.

We handhold you:

Our Home Loan Counselors (fleet-on-street) will provide you with ‘door-step service’, from filling out applications to collecting required documents and rigorously following up with Bank authorities to get sanction and disbursal of your Balance Transfer loan.

PropSeva® is a leading knowledge-based real estate services portal in fusion with

M Sri Fintech, a new-generation Fintech Company, offers the best domain knowledge, expert professional advice, the latest AI-based technology, and a ‘delighting the customer’ approach with door-step services.

Contact: Rajendra Deshpande

M: 91 96868 56707/93412 13530 | E: office@propseva.com, deshpande@propseva.com